✈️Air Taxi and Mobility Industry

A 30,000 Foot Overview

Happy Thursday everyone,

Today we're venturing slightly outside our usual simplicity investing principles to explore an emerging sector with long-term potential: the future air mobility (FAM) industry.

While we focus on straightforward investment approaches, occasionally we spot opportunities in more complex, developing markets that warrant attention.

The electric vertical takeoff and landing (eVTOL) sector represents one such opportunity - a nascent industry approaching commercialization despite funding challenges, with companies like Archer (red logo) and Joby Aviation (blue logo) positioning themselves at the forefront of urban air mobility revolution.

As with any emerging technology, these investments carry substantial risk, but their potential upside within a balanced portfolio makes them worth understanding.

Industry Overview and Funding Trends

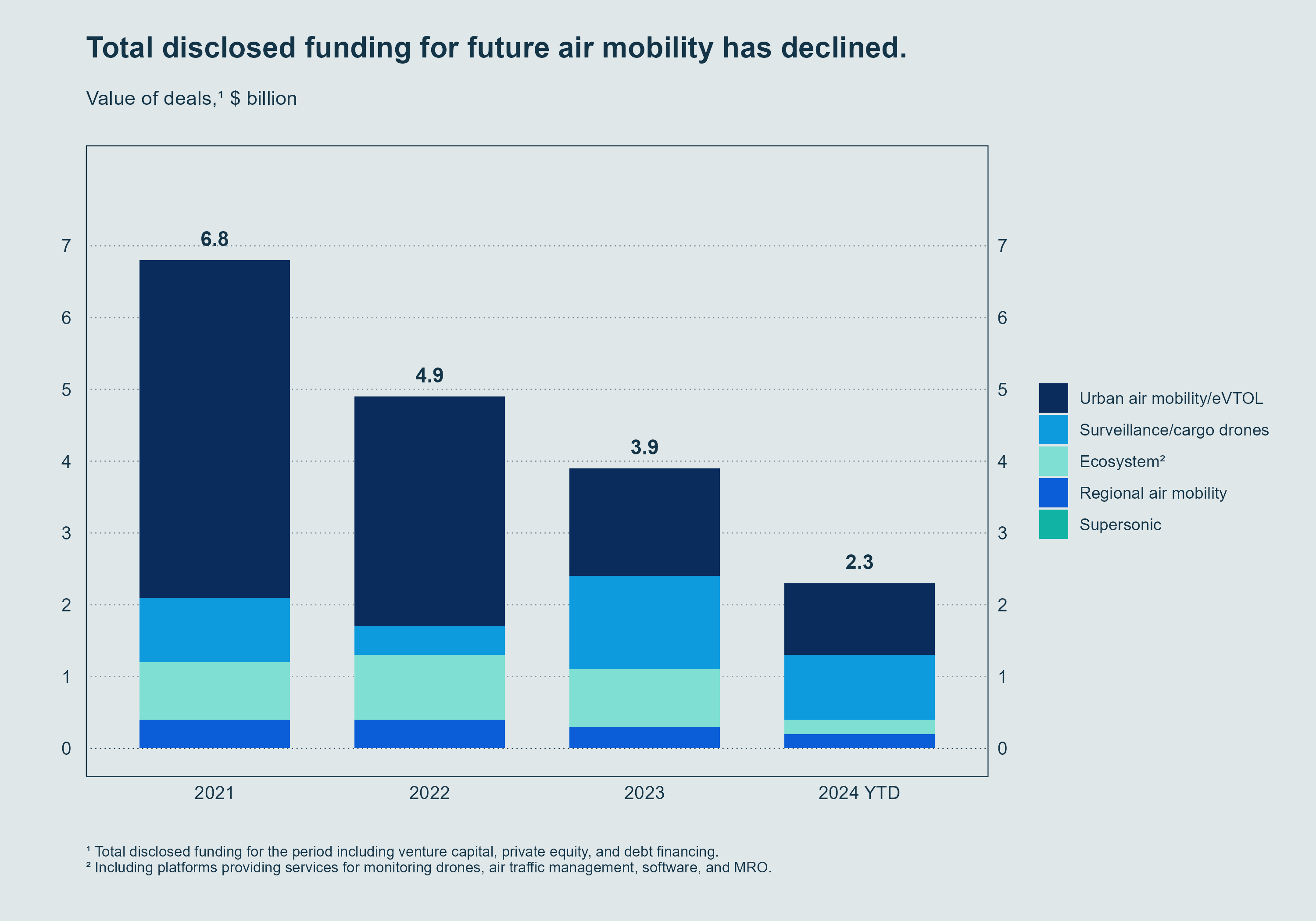

The future air mobility (FAM) industry, which includes electric vertical takeoff and landing (eVTOL) aircraft, surveillance/cargo drones, sustainable aviation, and supersonic aircraft, is approaching commercialization amid declining funding. Disclosed funding has decreased significantly from its 2021 peak of $6.8 billion to approximately $3.9 billion in 2023, with 2024 expected to maintain similar levels (about $2.5 billion announced by August).

Historically, funding has concentrated on urban air mobility (UAM) projects, particularly eVTOL aircraft, with surveillance/cargo drones ranking second. Together with cargo drones, these segments account for nearly 80% of publicly disclosed FAM funding in 2024. The order backlog remains substantial, with approximately 35,500 aircraft orders valued at $168 billion, demonstrating strong market interest despite funding challenges.

Segment-Specific Challenges

The eVTOL sector faces particularly acute challenges as companies approach certification and commercialization.

Many companies have full-scale prototypes flying, with some (like AutoFlight and EHang in China) already receiving type certification, while others (Archer, Joby) target certification within 18 months. However, most players require significant additional funding (typically $1-2 billion) to complete development, testing, and certification processes.

Even after certification, eVTOL manufacturers will need substantial capital to develop manufacturing capabilities and build initial fleets. Traditional asset-backed financing remains unavailable for these unproven aircraft, and manufacturing programs tend to be cash-negative for years post-certification.

Aircraft orders also show changing patterns, with 2023 recording 4,800 new orders (worth $22 billion), a 32% decrease from 2022. The current backlog involves 21,300 aircraft worth approximately $118 billion, though industry experts acknowledge many orders may not materialize due to technical challenges or financial constraints.

Future Outlook

This report indicates cautious optimism for the FAM industry, while acknowledging upcoming challenges:

Industry consolidation is expected, with mergers, acquisitions, and some closures as the sector matures

Expansion of infrastructure (charging facilities, landing sites) will need to accelerate to support commercial operations

Drone deliveries are projected to grow substantially in retail, prepared food, and critical product delivery segments

The electric vertical takeoff and landing (eVTOL) industry is approaching a critical juncture in 2025, with several major players working toward certification and commercial operations. While many companies had targeted 2025 for launching passenger services, the challenging investment climate and lengthy FAA certification process have created hurdles for meeting these ambitious timelines.

Archer Aviation

Archer Aviation Inc. (NYSE: ACHR) a leader in electric vertical takeoff and landing (eVTOL) aircraft, today announced the FAA issued for public inspection the final airworthiness criteria for Archer’s Midnight aircraft.

Archer Aviation is an exciting company that's developing a new method of urban transportation. Its upside potential is huge -- Morgan Stanley projects that the urban air mobility market could reach $1 trillion by 2040.

The company is making solid progress and has taken pre-delivery payments for 1,141 aircraft. The United Arab Emirates leads the way with 475 orders, followed by the United States (300) and India (200). The total value of its order book is up to $5.71 billion, and it has received deposits of $26 million on these orders, so it has a huge pile of potential cash flow awaiting it.

However, the company is still in the early stages of its growth story and given that it is a pre-revenue and pre-commercial business, a significant amount of execution risk remains. Any hiccups in testing or manufacturing its aircraft could affect its timelines, pushing back the point at which it can begin making deliveries and recognizing revenue.

Archer Aviation

Partnered with Stellantis and Southwest Airlines

Completed construction of 400,000 sq ft manufacturing facility in Covington, GA

Planning production starts in early 2025

Targeting 650 aircraft annually by 2030

Raised $300M from institutional investors including BlackRock

Received FAA Part 141 certification for pilot training

Total liquidity position of ~$1B

Joby Aviation

Joby (NYSE: JOBY) also recently received its Part 145 Repair Station Certificate from the FAA, allowing the Company to perform select maintenance activities on aircraft and marking another key step on the path to commercializing Joby’s electric air taxi service.

December 2024 Joby is the first eVTOL manufacturer to complete three of five stages of the FAA type certification program and is more than 40 percent complete with the Company’s work for the fourth stage.

Joby Aviation

Partnered with Toyota and Delta Air Lines

Completed first three of five FAA certification phases

Plans to begin flight testing for type inspection authorization (TIA)

Targeting initial operations in 2025

Secured $500 million additional funding from Toyota

Partnered with Atlantic Aviation for charging infrastructure in NY and LA

First to conduct an electric air taxi flight in NYC (November 2023)

Joby introduced ElevateOS software suite for passenger booking

Charting the Path Forward

As funding patterns shift and the industry matures, investors will likely concentrate on FAM players demonstrating clear paths to certification, production, and proven customer demand. While challenges remain, particularly around securing adequate funding for commercialization, the report suggests that companies with strong business models and technological progress can successfully navigate this crucial transition period.

The industry appears to be consolidating around a "big three" of Beta Technologies, Joby Aviation, and Archer Aviation.

While 2025 may not see widespread commercial operations as initially hoped, significant progress is being made in certification, infrastructure development, and pilot training. Early operations are likely to focus on specific routes and markets, with Dubai and Abu Dhabi emerging as potential early adopters.

Archer and Joby Aviation stocks are best-suited for investors who have a high tolerance for risk and a long-term investing horizon. Further, if you choose to buy it, your holdings should be a modest-sized part of a balanced portfolio; don't risk more money on Archer or Joby Aviation stock than you're willing to lose.