Presidents Do Not Matter

Much........................

When we say this, we are alluding to long-term returns in the market.

There is convincing evidence in a two-factor model (unemployment and valuations) that relate to long-term stock market returns.

The below histograms show the average returns for where we are now:

CAPE 10 is at about 37

Unemployment is at 4.1%

The average return for the left chart at CAPE 10 greater than 31 is -1.0% and the unemployment rate average return at between 2% and 5% is 2%. The blue histograms are the best gauge.

Mostly policies create noise and volatility. Are there lasting effects, sure. Too much fiscal spending can create issues or too little. Tax policy certainly matters and can propel or damper inflation. Trump’s 2016 corporate policy get little credit for a jump in corporate profits after tax. His saber rattling of tariffs will have a negligible impact. When you look at the chart below you see the USA is the lowest in the G20. This is a weighted average of all goods.

So what really matters then? We have long had a philosophy of

LIFE

Liquidity

Interest Rates

InFlation

Earnings/Economic growth are the key components.

So who controls those levers? The Fed mostly controls short interest rates and liquidity through monetary policy. In addition the Fed can put push bank reserves up by providing banks with the capacity for additional lending through open market purchases.

Long term rates are market driven and inflation expectations.

Inflation can be two sources – demand driven consumer, business and government spending out pacing supply of goods and services or supply driven a shock to supply chains like we saw during COVID.

The prior demand driven was seen as two demographics collide:

Boomers and Millennials in addition to a flood of liquidity from government spending. This pushed savings into the hands of consumers, pushing inflation to record levels not seen since the 1970s.

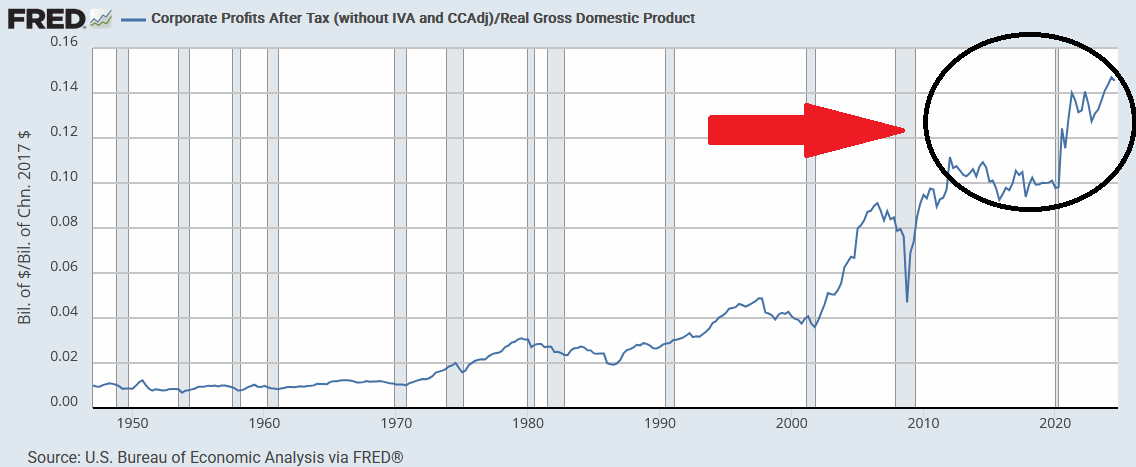

Earnings were propelled thorough spending and the Trump tax cuts in 2017. As you can see by the below chart profits have been elevated for 15 years only slowing during COVID.

Again, an extended period of near zero interest rates has caused an unsustainable corporate profit margin.

Of course, this is a simplified look at the economy and markets but presidents do not control these factors to any large degree.

Congress controls the budget which can have an impact on debt and deficits which may lead to influencing long term rates. Short term stimulus can impact inflation which is usually transitory. In the case of current inflation the problem of two demographics will not go away for years and the only tangible way to lower inflation when demand is sticky is to slow the economy.

The current situation with interest rates is that years of zero rates and a low ten-year treasury has pushed housing prices to some of the lowest affordability issues in history. This has been the case with asset prices in the last ten years.

Too much liquidity and zero rates have caused asset price inflation not consumer price inflation unit recently.

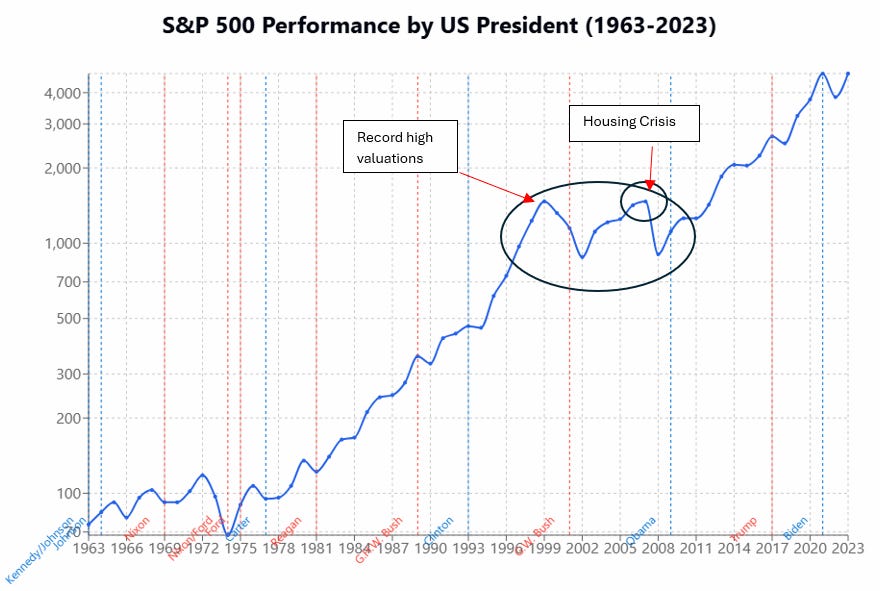

I might add that the housing crisis was a combined effort of congress passing a bill that allowed low or no down payments fueled by Wall Street leveraging that into the now famous CDO market.

In 1992, the Democratic Congress approved the Affordable Housing Act. This act eventually led to a lot of bad loans for people that should have never been able to enter the housing market. Government-sponsored enterprises Fannie Mae and Freddie Mac were to become deeply involved in this, the Affordable Housing Act, and were pushing bad loans to comply with the government mandate. Democrats Rep. Barney Frank and Sen. Chris Dodd were the leaders for this mandate.

Our conclusion is that the Fed matters most and congressional policy (the spending purse) can have a lasting impact but in the end valuations matter most being pushed around by liquidity, interest rates, inflation and earnings.